Slide transcript

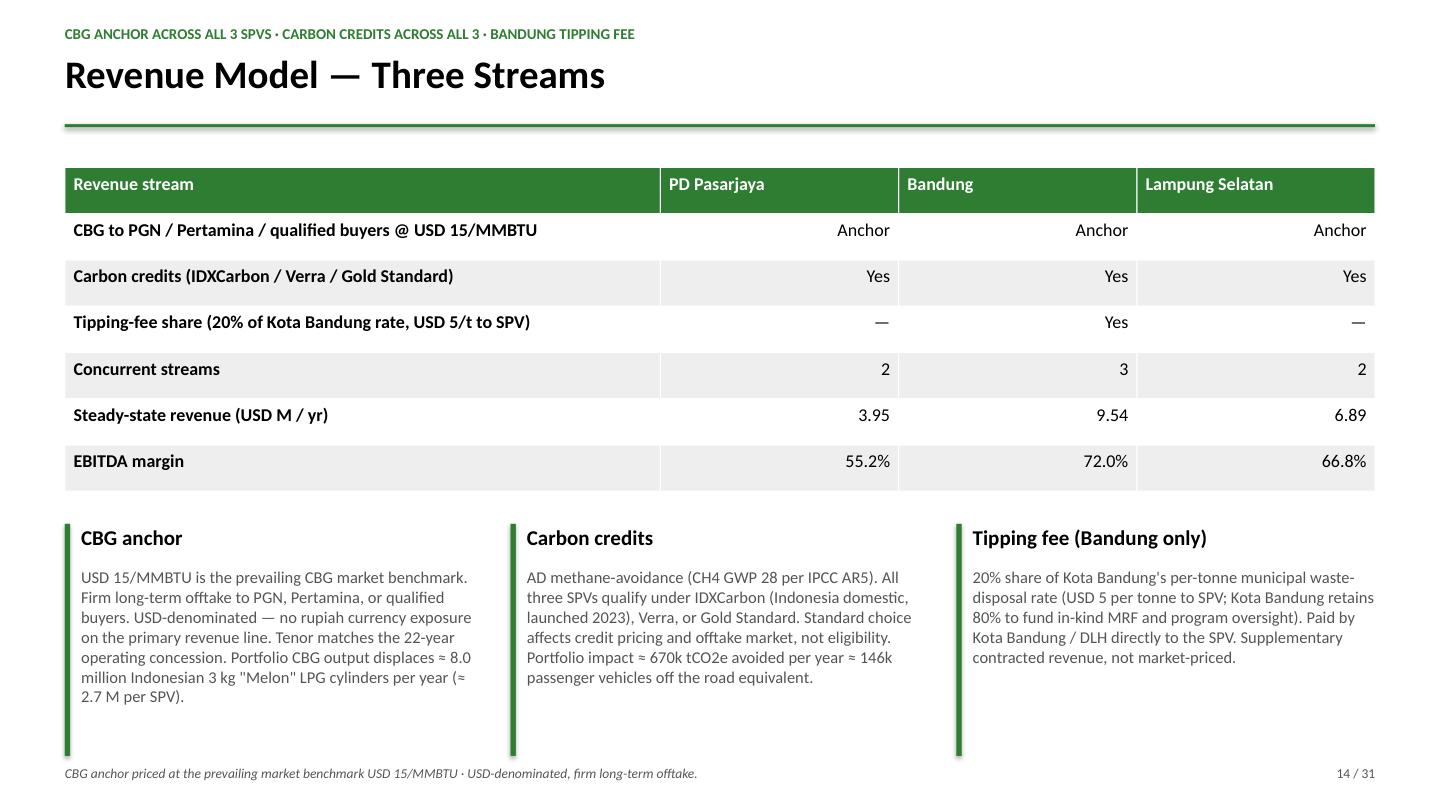

| Revenue stream | PD Pasarjaya | Bandung | Lampung Selatan |

|---|---|---|---|

| CBG to PGN / Pertamina / qualified buyers @ USD 15/MMBTU | Anchor | Anchor | Anchor |

| Carbon credits (IDXCarbon / Verra / Gold Standard) | Yes | Yes | Yes |

| Tipping-fee share (20% of Kota Bandung rate, USD 5/t to SPV) | — | Yes | — |

| Concurrent streams | 2 | 3 | 2 |

| Steady-state revenue (USD M / yr) | 3.95 | 9.54 | 6.89 |

| EBITDA margin | 55.2% | 72.0% | 66.8% |

CBG anchor

Carbon credits

Tipping fee (Bandung only)

USD 15/MMBTU is the prevailing CBG market benchmark. Firm long-term offtake to PGN, Pertamina, or qualified buyers. USD-denominated — no rupiah currency exposure on the primary revenue line. Tenor matches the 22-year operating concession. Portfolio CBG output displaces ≈ 8.0 million Indonesian 3 kg "Melon" LPG cylinders per year (≈ 2.7 M per SPV).

AD methane-avoidance (CH4 GWP 28 per IPCC AR5). All three SPVs qualify under IDXCarbon (Indonesia domestic, launched 2023), Verra, or Gold Standard. Standard choice affects credit pricing and offtake market, not eligibility. Portfolio impact ≈ 670k tCO2e avoided per year ≈ 146k passenger vehicles off the road equivalent.

20% share of Kota Bandung's per-tonne municipal waste-disposal rate (USD 5 per tonne to SPV; Kota Bandung retains 80% to fund in-kind MRF and program oversight). Paid by Kota Bandung / DLH directly to the SPV. Supplementary contracted revenue, not market-priced.