Slide transcript

BASE 70/30 WELL ABOVE 1.30X DSCR FLOOR · ALL SPVs HOLD 85/15 WITH COMFORTABLE HEADROOM

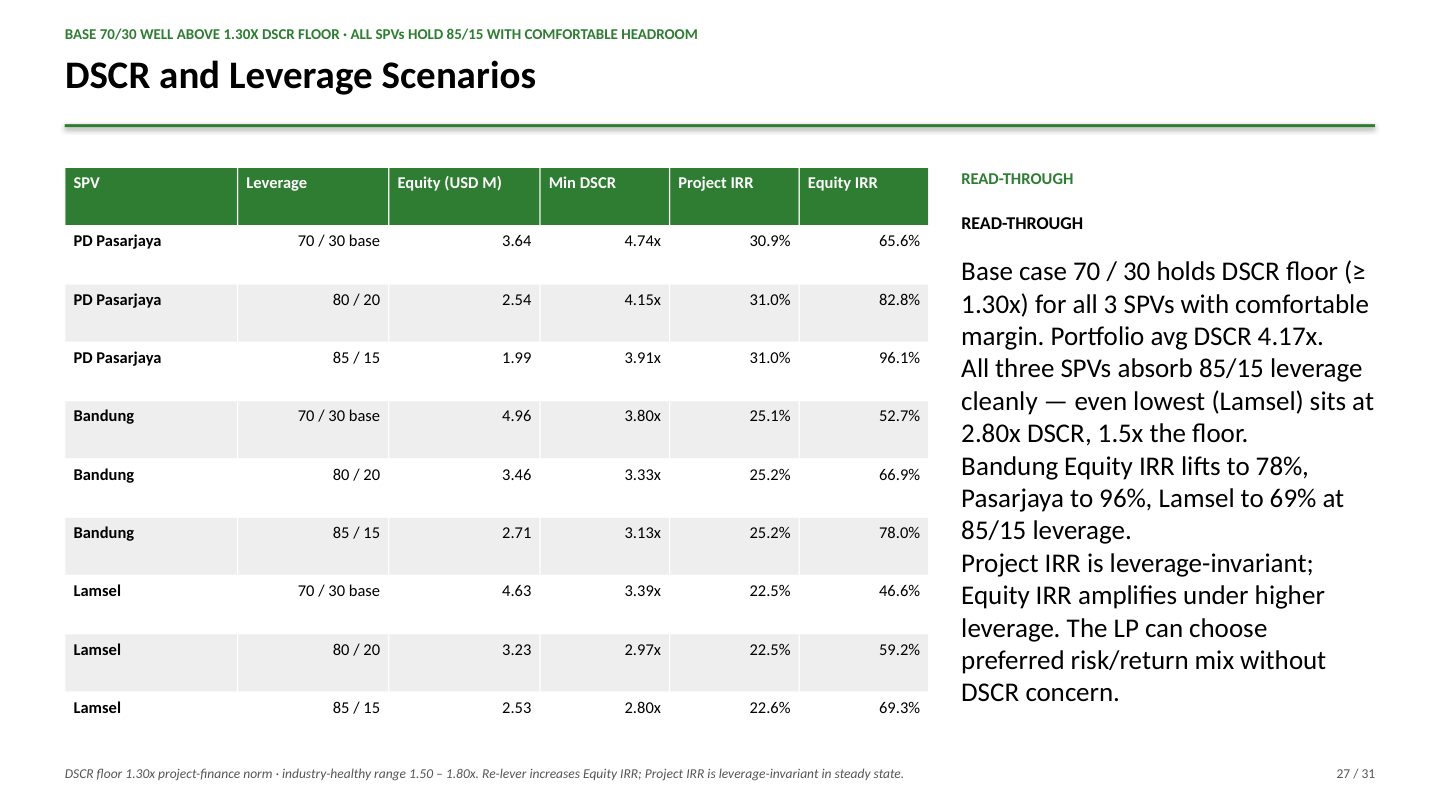

| SPV | Leverage | Equity (USD M) | Min DSCR | Project IRR | Equity IRR |

|---|---|---|---|---|---|

| PD Pasarjaya | 70 / 30 base | 3.64 | 4.74x | 30.9% | 65.6% |

| PD Pasarjaya | 80 / 20 | 2.54 | 4.15x | 31.0% | 82.8% |

| PD Pasarjaya | 85 / 15 | 1.99 | 3.91x | 31.0% | 96.1% |

| Bandung | 70 / 30 base | 4.96 | 3.80x | 25.1% | 52.7% |

| Bandung | 80 / 20 | 3.46 | 3.33x | 25.2% | 66.9% |

| Bandung | 85 / 15 | 2.71 | 3.13x | 25.2% | 78.0% |

| Lamsel | 70 / 30 base | 4.63 | 3.39x | 22.5% | 46.6% |

| Lamsel | 80 / 20 | 3.23 | 2.97x | 22.5% | 59.2% |

| Lamsel | 85 / 15 | 2.53 | 2.80x | 22.6% | 69.3% |

READ-THROUGH

READ-THROUGH

Base case 70 / 30 holds DSCR floor (≥ 1.30x) for all 3 SPVs with comfortable margin. Portfolio avg DSCR 4.17x.

All three SPVs absorb 85/15 leverage cleanly — even lowest (Lamsel) sits at 2.80x DSCR, 1.5x the floor.

Bandung Equity IRR lifts to 78%, Pasarjaya to 96%, Lamsel to 69% at 85/15 leverage.

Project IRR is leverage-invariant; Equity IRR amplifies under higher leverage. The LP can choose preferred risk/return mix without DSCR concern.

DSCR floor 1.30x project-finance norm · industry-healthy range 1.50 – 1.80x. Re-lever increases Equity IRR; Project IRR is leverage-invariant in steady state.