Slide transcript

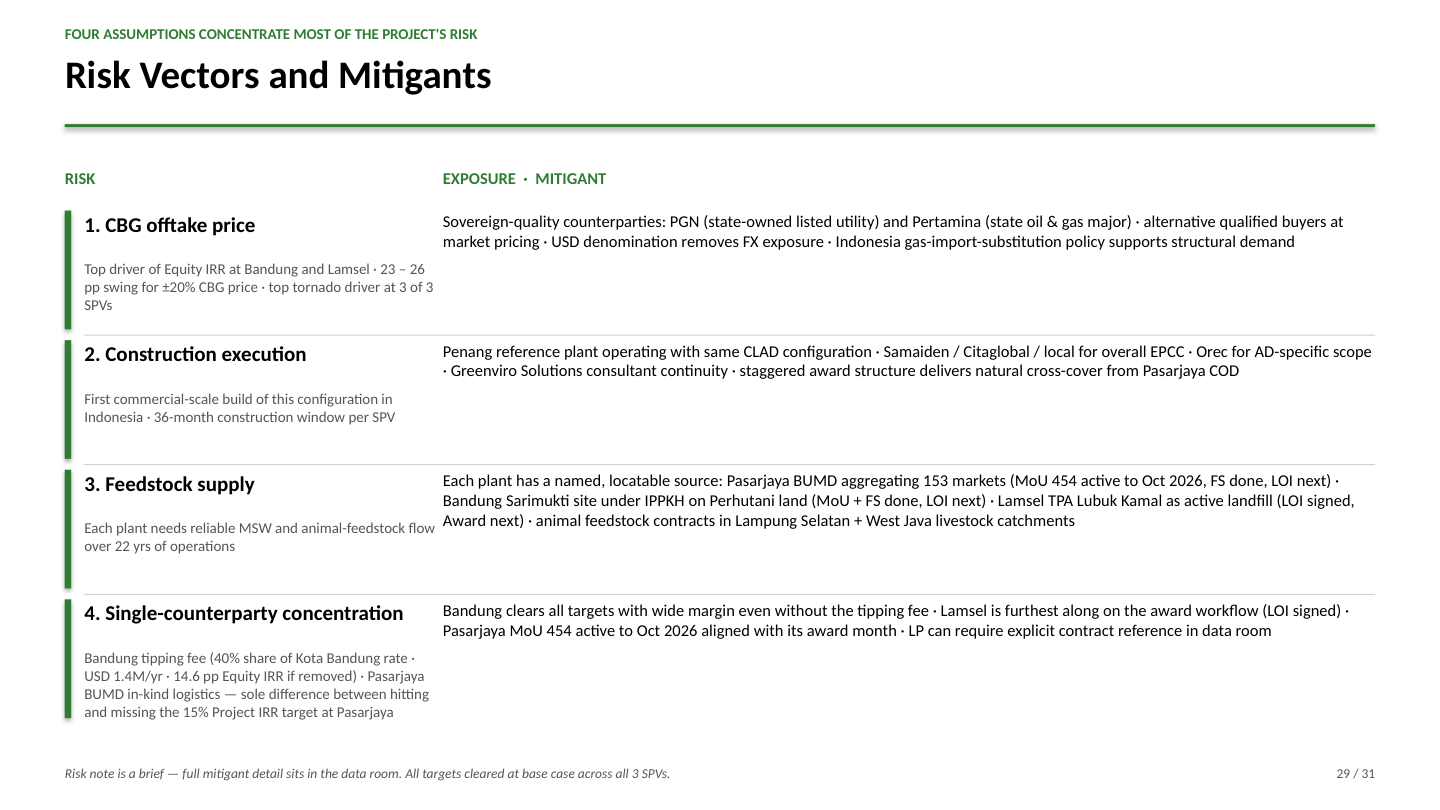

RISK

EXPOSURE · MITIGANT

1. CBG offtake price

Sovereign-quality counterparties: PGN (state-owned listed utility) and Pertamina (state oil & gas major) · alternative qualified buyers at market pricing · USD denomination removes FX exposure · Indonesia gas-import-substitution policy supports structural demand

Top driver of Equity IRR at Bandung and Lamsel · 23 – 26 pp swing for ±20% CBG price · top tornado driver at 3 of 3 SPVs

2. Construction execution

Penang reference plant operating with same CLAD configuration · Samaiden / Citaglobal / local for overall EPCC · Orec for AD-specific scope · Greenviro Solutions consultant continuity · staggered award structure delivers natural cross-cover from Pasarjaya COD

First commercial-scale build of this configuration in Indonesia · 36-month construction window per SPV

3. Feedstock supply

Each plant has a named, locatable source: Pasarjaya BUMD aggregating 153 markets (MoU 454 active to Oct 2026, FS done, LOI next) · Bandung Sarimukti site under IPPKH on Perhutani land (MoU + FS done, LOI next) · Lamsel TPA Lubuk Kamal as active landfill (LOI signed, Award next) · animal feedstock contracts in Lampung Selatan + West Java livestock catchments

Each plant needs reliable MSW and animal-feedstock flow over 22 yrs of operations

4. Single-counterparty concentration

Bandung clears all targets with wide margin even without the tipping fee · Lamsel is furthest along on the award workflow (LOI signed) · Pasarjaya MoU 454 active to Oct 2026 aligned with its award month · LP can require explicit contract reference in data room

Bandung tipping fee (40% share of Kota Bandung rate · USD 1.4M/yr · 14.6 pp Equity IRR if removed) · Pasarjaya BUMD in-kind logistics — sole difference between hitting and missing the 15% Project IRR target at Pasarjaya